organization, but assertiveness is still one of the points to be developed.

Furthermore, leaders agree that they need to look for more robust tools to support a budgeting process with a higher level of analysis.

This is when companies come to Value Bridge asking for help in implementing an improvement in their traditional budgeting process.

We have a number of methodologies in our knowledge base, but typically an OBZ project has the following steps:

We analyze the last few years of the budget to identify seasonal patterns, key areas, main expenditures and also the alignment of these expenditures with the strategy.

At this stage we consolidate relevant market information for a good analysis of spending.

In addition to refining the chart of accounts and the cost center structure, some expense groupings are proposed along with the designation of a corporate officer.

One example is travel expenses, including tickets, accommodation and meals, where a person is responsible for ensuring that all areas apply the established rules, generating alignment in the forecasting of this “expense package”. Every month, the person responsible for this package will analyze any deviations and plan corrections.

As with the traditional budget, this document is a detailed guide to budgeting. The Guidelines Letter sets out contract adjustment indexes, inflation projections and general guidelines for the budgeting process. Often, the Guideline Letter has attached to it the definition of the type of expenditure envisaged in each accounting account and guidelines for quantifying this expenditure.

At this stage, each area is responsible for drawing up the budgets for their respective cost centers or “budget units”, following the guidelines in the Charter of Guidelines.

Some benchmarks are provided at this point, as a way of bringing productivity aspects to light. This stage characterizes much of Zero-Based Budgeting (ZBB), as each area will be making its budget based on its needs and not just on historical expenses.

When a company is looking to optimize the alignment of its budget with its strategies, one of the options is to adopt a methodology for prioritizing costs and expenses. This type of budget has 2 stages prior to decision-making, which allow for an even more in-depth understanding of the proposed budget.

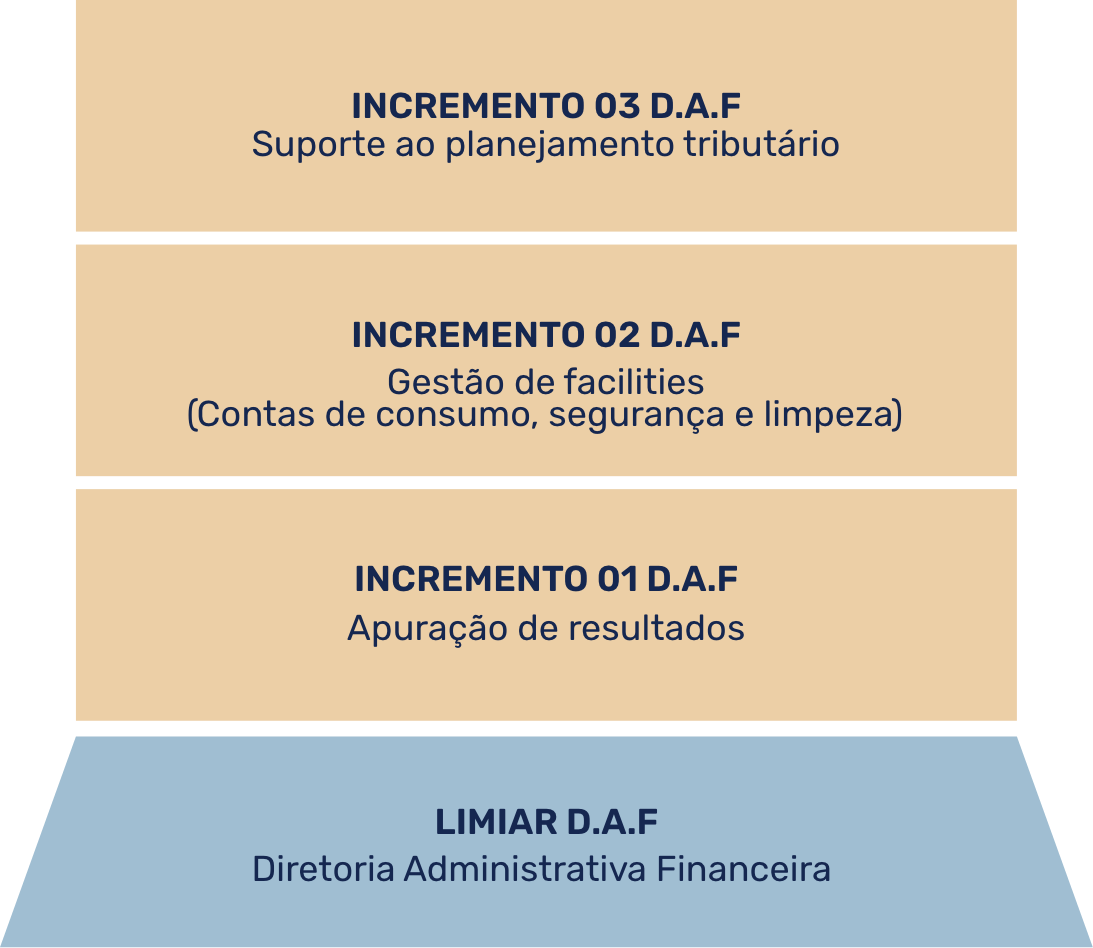

Segmentation of expenses into “increments”, which are blocks of expenses related to a clear “deliverable”.

The most important increment is placed as the “threshold” and is at the bottom of the tower. The other increments are then added in the shape of a tower, with the more strategic ones closer to the base of the tower and the less strategic ones further away from the base.

In the figure opposite is an example of a tower for the budget unit (BU) Financial Administrative Department

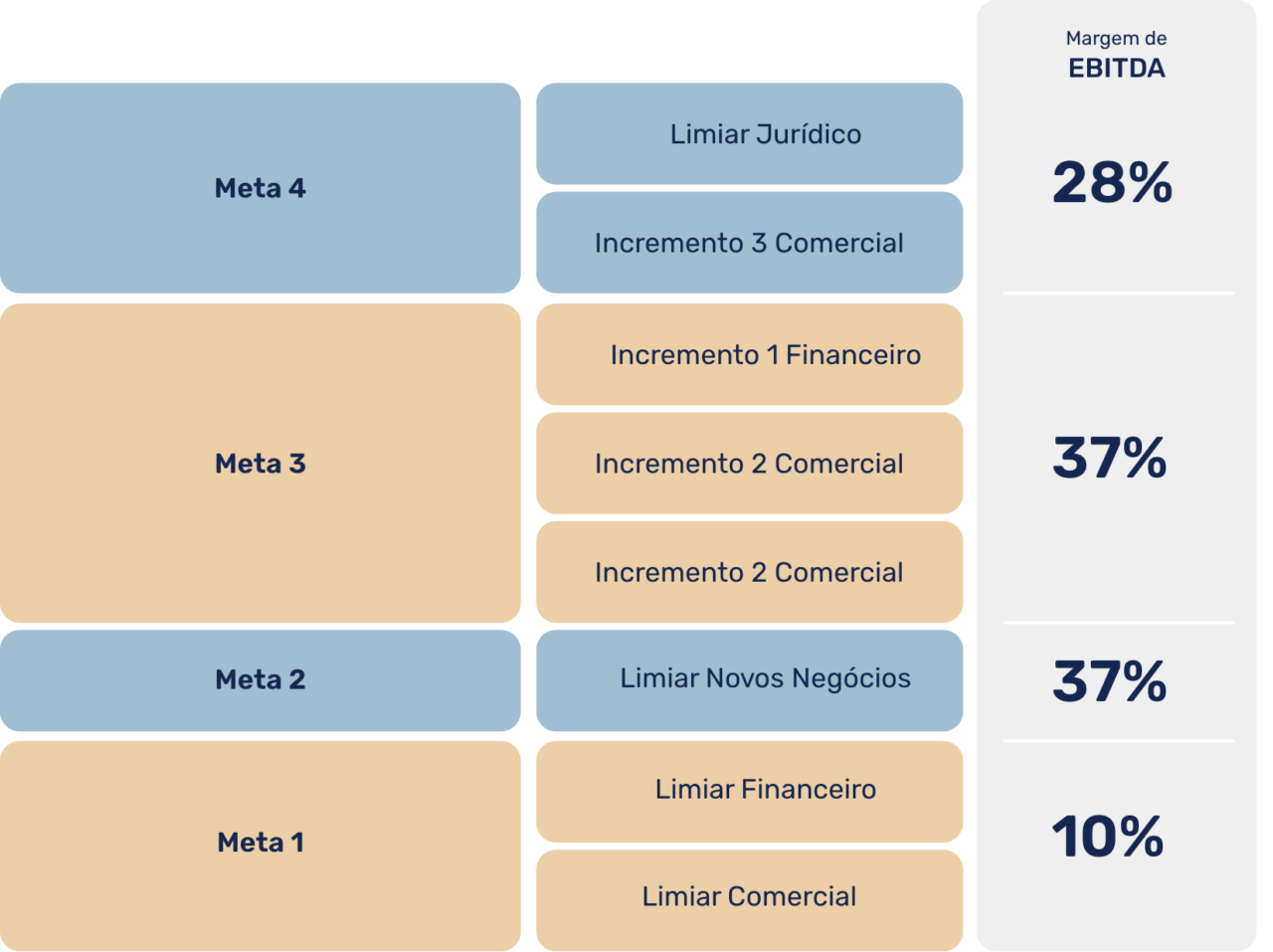

Segmentation of expenses into “increments”, which are blocks of expenses related to a clear “deliverable”.

The increments from all areas are then grouped according to strategy and positioned at the base of the tower. For each of the targets set, the resulting EBITDA margin can be calculated, as shown below:

In the Budget Prioritized by Strategies, by organizing the budgets of each area into prioritization towers, the strategic focus is stimulated, directing budget resources in an optimized way, when compared to other existing models.

Learn more about Value Bridge’s budgeting methodologies, our success stories and how we can be a value bridge for your business.